As Budget 2026 unfolds, individuals and businesses alike are closely examining the latest tax proposals that could shape financial planning and economic behavior for the year ahead. From revised income tax slabs to changes in deductions and compliance norms, this year’s budget brings a set of significant updates that taxpayers cannot afford to overlook. In this blog, we break down the most impactful tax reforms introduced in Budget 2026 — explaining what they mean, who they affect, and how you can prepare to make the most of them.

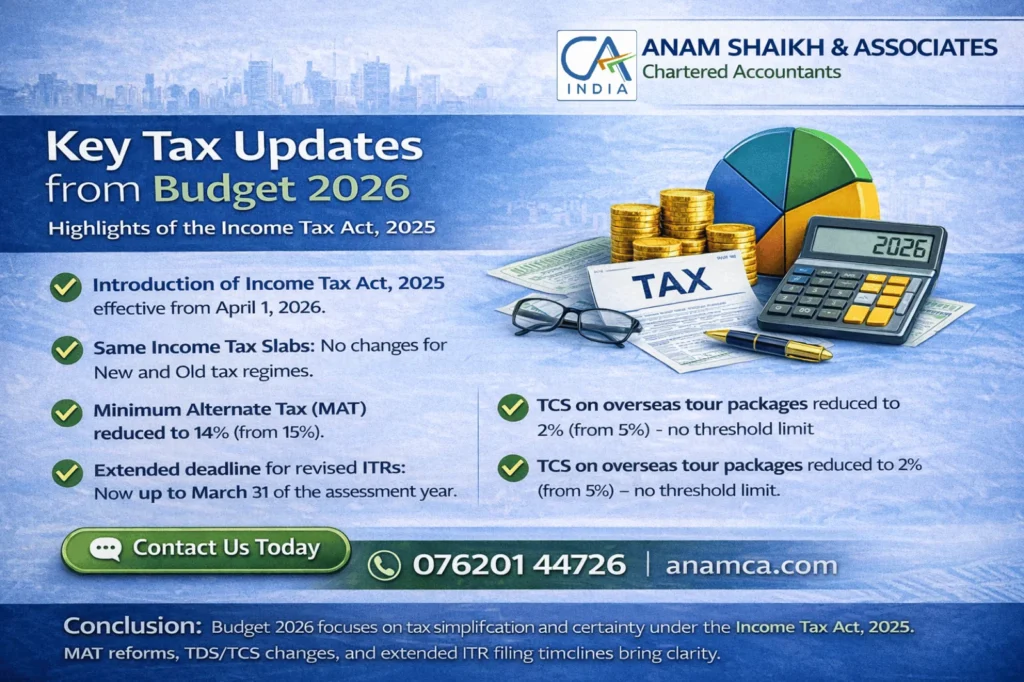

1. Introduction of the New Income Tax Act, 2025:

The Income Tax Act, 2025 will come into force from April 1, 2026 (AY 2027-28 onwards).

This replaces the Income Tax 1961 Act with a streamlined version (sections reduced significantly), simpler rules, redesigned forms, and ITR formats to be notified soon for better taxpayer preparation.

2. Income Tax Slabs and Rates:

No Changes : Slabs and rates remain unchanged under both new and old regimes for FY 2026-27 (AY 2027-28).

New Tax Regime Slabs (continuing):

Up to ₹4 lakh : 0%

₹4–8 lakh : 5%

₹8–12 lakh : 10%

₹12–16 lakh : 15%

₹16–20 lakh : 20%

₹20–24 lakh : 25%

Above ₹24 lakh : 30%

Income up to ₹12 lakh effectively tax-free (with Section 87A rebate up to ₹60,000); for salaried, up to ₹12.75 lakh after standard deduction.

Standard Deduction: ₹75,000 (new regime); ₹50,000 (old regime) – no increase announced.

Rate Reduction: MAT rate on book profits lowered from 15% to 14% (plus surcharge and cess).

MAT as Final Tax: From April 1, 2026 (AY 2027-28 onwards), MAT becomes the final tax liability for applicable companies.

No carry-forward or set-off of MAT credit against future tax liabilities.

This structural change provides long-term tax certainty and reduces litigation over credit claims.

Exemption for NRIs: Non-Resident Indians fully exempted from MAT.

Applicability : Continues for domestic companies not opting for concessional regimes (e.g., under Sections 115BAA/115BAB, which remain MAT-exempt).

Transition : Old regime (15% with credit) applies for pre-April 2026 assessments; companies should reassess book profit planning due to loss of credit mechanism.

4. ITR Filing and Compliance Timelines:

Extended Deadline for Revised and Belated ITRs:

Time limit for filing revised returns (Section 139(5)) and belated returns (Section 139(4)) extended from December 31 to March 31 of the assessment year.

Subject to a nominal fee (details to be notified).

This grants an extra three months for corrections, omissions, or incorporating new information, easing compliance and reducing disputes.

Original ITR Filing Deadlines (Staggered):

ITR-1 and ITR-2 (salaried individuals, simple income sources): Remains July 31 of the assessment year – no change for continuity.

Non-audit business cases, trusts, and complex returns (e.g., ITR-3, ITR-4, ITR-5, ITR-6, ITR-7 without audit): Extended to August 31 of the assessment year.

This decongests the filing season and allows more preparation time for businesses/trusts.

Audit-Related Deadlines: Unchanged – tax audit reports and related ITRs due by October 31 (or as existing).

Applicability : These changes apply prospectively (likely AY 2027-28 onwards, aligned with the new Act). For AY 2026-27, old timelines continue unless clarified. Late fees (Section 234F), interest (Section 234A), etc., may still apply for delayed filings.

5. Exemptions and Relief Measures:

Interest awarded by Motor Accident Claims Tribunal (MACT) to natural persons now fully exempt from income tax; related compliance simplified/eliminated.

Automated nil/lower TDS certificates for small taxpayers with multiple securities to ease deduction burdens and improve cash flow.

6. Tax Collected at Source (TCS) Reductions:

Overseas tour packages : TCS rate reduced to 2% (from 5%/20%), no threshold limit.

Education and medical remittances under LRS : TCS rate lowered to 2% (from 5%).

7. Tax Deducted at Source (TDS) Amendments:

Manpower supply services explicitly covered under contractor TDS provisions (rates 1%/2%) to remove ambiguity.

Other procedural simplifications to reduce litigation.

8. Securities Transaction Tax (STT):

On futures : Increased to 0.05% (from 0.02%).

On options : Increased to 0.15% (from 0.01%).

Aimed at moderating speculative trading in derivatives.

9. Other Notable Provisions:

20-year tax holiday (until 2047) for foreign cloud providers investing in Indian data centers to boost digital infrastructure.

No expansions in Section 80C deductions or major new exemptions – consistent with push toward the new regime.

Conclusion

Budget 2026 continues the government’s focus on tax simplification and certainty, highlighted by the introduction of the Income Tax Act, 2025 and rationalised compliance timelines. While tax slabs remain unchanged, key reforms in MAT, TDS/TCS, and filing procedures offer greater clarity and ease for taxpayers. Individuals and businesses should review these changes early and align their tax planning for AY 2027–28 to stay compliant and prepared.

We wish to consistently build value for our clients by delivering a motivated and committed team of professionals working hand in hand to maintain the highest standards of integrity and confidentiality in fulfilling client-specific needs.