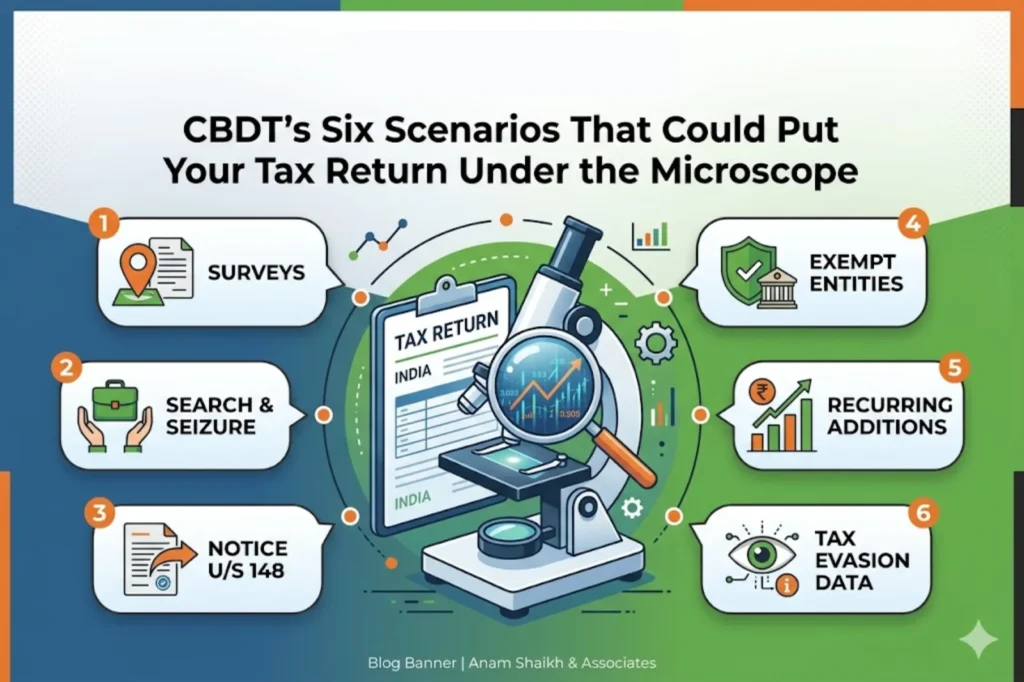

CBDT’s Six Scenarios That Could Put Your Tax Return Under the Microscope

Helping Startups Manage Finance, Compliance & Growth

04/28/2026

Tax Deducted at Source (TDS) and Tax Collected at Source (TCS) are very similar concepts, however TCS has several important distinctions. Tax Deducted at Source (TDS) refers to the amount of tax withheld from a payment made by a contract’s recipient. On October 1, 2018, with a few exceptions, all online merchants will be required to collect TCS. In this piece, we’ll break down how TCS relates to GST.

Take, as an illustration: When a vendor sells its wares or provides its services over an e-commerce platform and the operator collects payment from the vendor, this transaction is known as tax collection service (TCS).

By “TCS on GST,” we mean the GST that is deducted from the payment made to a vendor who makes a supply through an online marketplace on the operator’s behalf. TCS is determined by dividing net taxable supplies by TCS. Specifically, TCS under GST is addressed under Section 52 of the CGST Act.

Many thanks to the owners, managers, and operators of the various e-commerce platforms on which TCS relies. For TCS to apply, operators must collect client payments on behalf of vendors or suppliers. In other words, when remitting funds to sellers, e-commerce platforms must deduct TCS before transferring the remaining funds.

Certain e-commerce platform services are exempt from the TCS rules, as listed below:

For instance, An individual business, Raj Stores, sells garments on the online marketplace Flipkart.

Because of its status as an e-commerce provider, Flipkart must withhold TCS from any consideration it collects on behalf of XYZ before transferring the funds to the latter.

After a 1% TCS reduction, online marketplaces will pay the dealers and traders who supply their goods and services.

In Notification No. 52/2018 issued under the CGST Act and Notification No. 02/2018 issued under the IGST Act, the CBIC made the rate official.

This means that for supplies made within the same state, TCS of 1% will be collected (0.5% under CGST and 0.5% under SGST). The IGST Act mandates that the TCS rates for interstate transactions be set at 1%.

The TCS payment is paid to the government by the e-commerce operator through the GSTR-8 Return. Could I get a refund for TCS Deducted?

To the extent that TCS is deducted by the E-Commerce Operator, the full amount should be credited to registered sellers through the E-Commerce Portal.

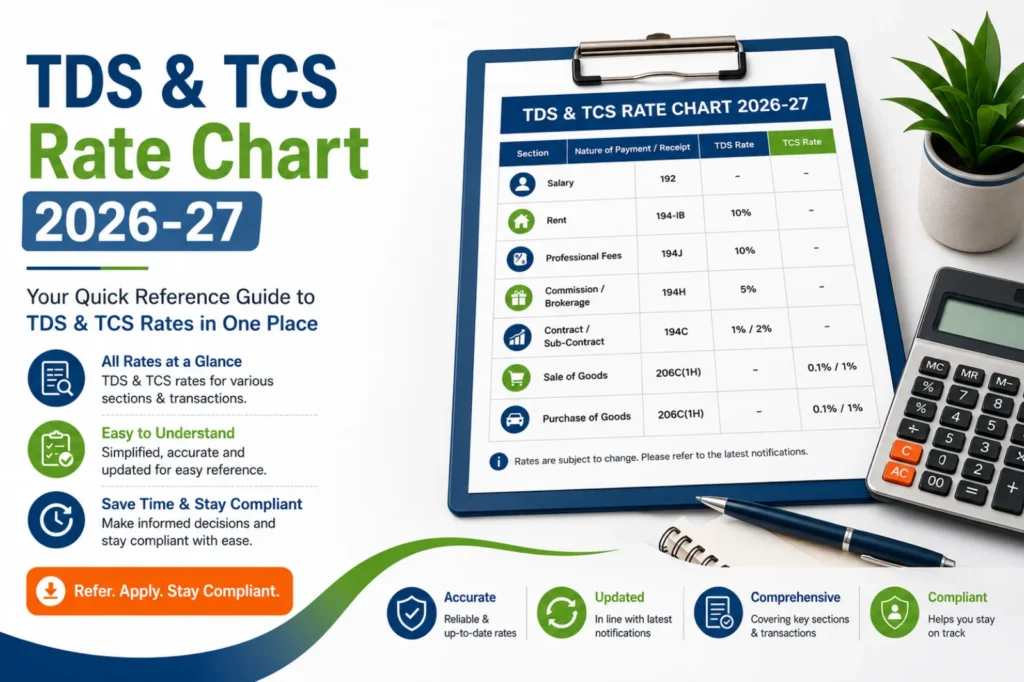

Types of Goods | Tax rates |

Product sales to a single customer totaling more than Rs. 50 million | 0.1% |

Timber woods under a forest lease or any other mode | 2.5% |

Tendu leaves | 5% |

Forest produces other than tendu leaves & timber | 2.5% |

Liquor of alcoholic nature, made for human consumption | 1% |

Minerals like lignite, coal & iron ore | 1% |

Purchase of motor vehicle exceeding Rs.10L | 1% |

Parking lot, Toll Plaza & Mining & Quarrying | 2% |

Registered Sellers of Electronic Commerce Portals can claim a complete refund of any TCS deducted from their sales by filing a “TDS and TCS Credit Receivable return” through the GST Portal.

Credit will be applied to your Cash Ledgers once the return is filed, and you may then use that money to pay any taxes owed.

Online marketplaces like Amazon, Flipkart, and Snapdeal had to revamp their online payment system and accounting practises in order to comply with TCS on GST.

They need to get GST registration in every state they do business in. To put these regulations into practice in regular companies, ERP systems must be well connected.

However, in order to conduct business on such marketplaces, E-tailers or sellers must first register for GST. In addition, until these suppliers complete their reports and collect the additional taxes, their working capital will be frozen if they provide through an e-commerce operator.

In many ways, GST tax deductions and credits are advantageous. In an effort to better regulate tax evasion, the government implemented TDS and TCS in GST. Tax deducted at source (TDS) and tax collected at source (TCS) under GST are addressed in Sections 51 and 52 of the CGST Act.

There would be an immediate update in the electronic books of the deductee or supplier once the deductor files their returns under the TDS system. This tax payment will be credited to the deductee’s electronic cash ledger where it can be used to pay other taxes whenever the deductee sees fit.

The use of TDS has proven to be a highly effective method of bringing previously unorganized sectors into compliance with tax regulations and reducing the likelihood of fraud.

TCS under GST also monitors online vendors, records financial dealings, and ensures that taxes are paid on schedule.

There is no threshold restriction for GST registration, thus all e-commerce businesses that are obligated to collect TCS must register. With a few exceptions, anyone selling a product through an e-commerce platform’s online marketplace must also be registered for GST.

In the month of supply, the final day of the month is the due date for TCS deposits. After the end of the month of supply, it will be deposited to the government’s credit within 10 days.

Here are the methods by which the tax is disbursed:

Before October 1, 2018, the effective date of implementing TCS regulations, online merchants must register with each state’s GST agency. Therefore, well-integrated ERP systems are required to smoothly execute these provisions in operational procedures.

In addition, until a vendor files their taxes and claims any overpayment, their working capital will be frozen if they sell through an e-commerce operator. Because of this, it’s possible that fewer small and medium-sized enterprises will use the platform to market and sell their wares and services.

The government claims that if taxes are taken out of every purchase, tax evasion will be drastically cut down.

All suppliers will have access to the data operators submit in GSTR 8 via GSTR 2A. If you miss the GSTR-8 deadline, don’t worry; you can access the materials in GSTR 2A. Please be aware that the GSTR-2B return will not include information about these credits.

Instead, suppliers’ electronic cash ledgers will record the tax payments they’ve received. After confirming their supplies are listed accurately in GSTR 2A, suppliers can submit a claim for the credit.

GSTR 8 returns cannot be changed after they have been submitted. Both the operator and the supplier will be informed of any discrepancies found while matching and reconciling supply data and GSTR 2A.

If the error is not fixed by the provider by the deadline, the supplier’s liability will increase by the tax amount. The difference, plus any applicable interest, is due from the vendor.

Learn Why Anam Shaikh & Associates Is The Best GST Software Available:

We wish to consistently build value for our clients by delivering a motivated and committed team of professionals working hand in hand to maintain the highest standards of integrity and confidentiality in fulfilling client-specific needs.

This will close in 0 seconds

WhatsApp us