RCM on Renting Commercial Property by Unregistered Persons to Registered Persons Under GST

10/09/2024

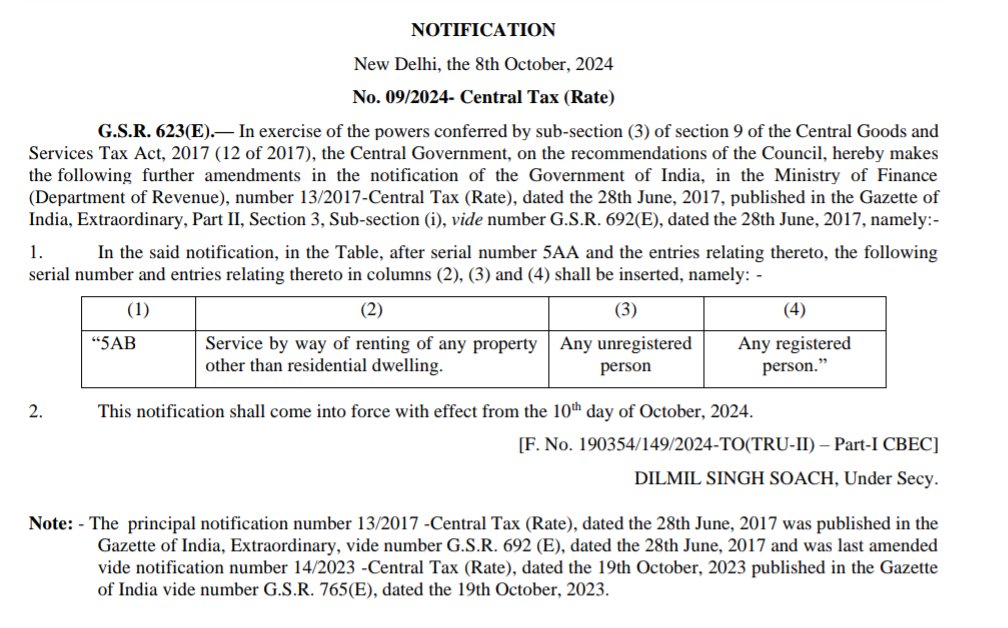

If you are a tenant and pay rentals for use of any commercial property in India and the owner of that commercial property is not registered under GST, then tax is payable under RCM i.e Reverse Charge Mechanism by Tenant. This is applicable with effect from 10th October, 2024.

Declaration is issued by The Principal notification number 13/2017 – Central Tax (Rate), date the 28th June, 2017 was published in the Gazette of India, Extraordinary, vide number G.S.R. 692 (E ), dated the 28th June, 2017 and was last amended vide notification number 14/2023 – Central Tax (rate), dated the 19th October, 2023 published in the Gazette of India vide number G.S.R 765 ( E ), dated the 19th October, 2023 vide Notification No. 09/2024 – Central Tax (Rate).

Notification No. 09/2024 – Central Tax (Rate) has issued Impact of Reverse Charge Mechanism (RCM) on Renting of Property (Other than Residential Dwellings) and applicable with effect from 10th October, 2024.

For Clear Understanding, we have tried to explain the notification issued above in Layman’s language as follows:

Unregistered Tenant & Unregistered Owner:

In this scenario, GST is not applicable neither Forward Charge Mechanism (FCM) nor Reverse Charge Mechanism (RCM) is triggered.

Unregistered Tenant & Registered Owner :

In this scenario, GST is applicable under the Forward Charge Mechanism (FCM), with the owner being responsible for charging and remitting GST to the Government.

Registered Tenant & Registered Owner:

In this scenario, GST is applicable under the Forward Charge Mechanism (FCM), with the owner responsible for charging and remitting GST to the Government.

Registered Tenant & Unregistered Owner:

In this scenario, GST is applicable under the Reverse Charge Mechanism (RCM), with the tenant being liable to pay and remit GST to the government.

Registered Tenant (Composition Taxpayer) & Any Owner:

If the tenant is a composition taxpayer, the GST liability under the Reverse Charge Mechanism (RCM) becomes an additional cost, as the tenant is not eligible to claim Input Tax Credit (ITC).

The above clarification outlines the tax liabilities for renting of Commercial properties in India under different registration statuses, ensuring compliance with prevailing GST provisions.

To get more information about the subject mentioned above, you can contact us at +91 76201 44726 or email us at anam_ca@yahoo.com. Our firm, Anam Shaikh & Associates, an audit firm in Mumbai, is a team of professionals and experts who care about all your compliances. We are an expert CA Firm in Mumbai for GST Return Filling in Mumbai, Income Return Filling in Mumbai Audit & Assurance Services, and accounting services in Mumbai.

We wish to consistently build value for our clients by delivering a motivated and committed team of professionals working hand in hand to maintain the highest standards of integrity and confidentiality in fulfilling client-specific needs.