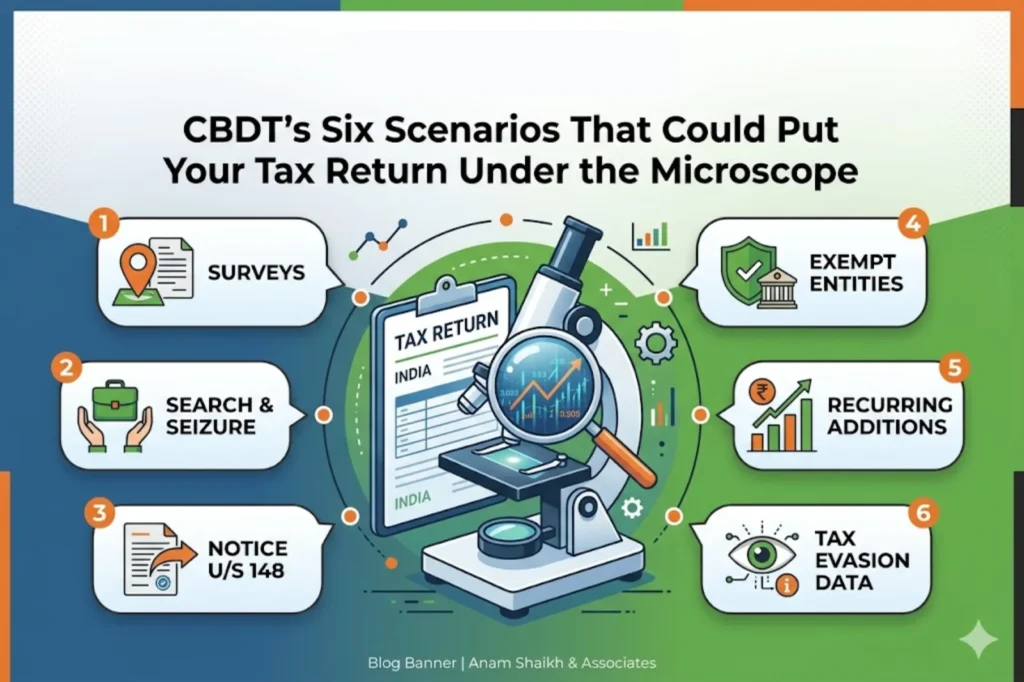

CBDT’s Six Scenarios That Could Put Your Tax Return Under the Microscope

Helping Startups Manage Finance, Compliance & Growth

06/07/2026

India’s Central Board of Direct Taxes (CBDT) has issued fresh guidelines prescribing the parameters and procedures for compulsory selection of income-tax returns for complete scrutiny during Financial Year 2026-27. Addressed to all Principal Chief Commissioners and Director Generals of Income-tax across the country, the circular defines six distinct scenarios which was termed “Systems Scenario Codes” under which a taxpayer’s return filed for FY 2025-26 will be mandatorily picked up for detailed examination.

Issued vide letter F.No.225/56/2026/ITA-II dated 4th June 2026 from Kartavya Bhawan, New Delhi, and signed by Dr. Indu Bala, Deputy Secretary to the Government of India, the guidelines draw their authority from Section 536(2)(c) of the Income-tax Act, 2025.

The guidelines are organised around six clearly defined selection parameters, each with a corresponding code and a prescribed procedure for how such cases are to be identified, notified, and processed.

Where a survey under Section 133A of the Income-tax Act, 1961 — other than a survey under Section 133A(2A) — has been conducted on or after 1 April 2024, the assessee’s return shall be compulsorily selected for scrutiny.

Selection will be made by the Directorate of Income-tax (Systems), with the approval of DGIT(Systems), Delhi, based on information provided by the Commissioner (OSD)(Investigation), CBDT. Notice u/s 143(2) will be served through the Prescribed Income-tax Authority or the concerned Assessing Officer.

Cases where a search u/s 132 has been initiated, or a requisition u/s 132A has been made, on or after 1 April 2024, are covered.

For searches initiated or requisitions made on or after 1 September 2024, the return shall be selected for the assessment year covered by Section 158BA(6) of the Act.

Selection is made by the Assessing Officer concerned with prior administrative approval of Pr.CIT/Pr.DIT/CIT/DIT.

(i) Search & seizure or survey on or after 1 April 2021 but before 1 September 2024: The JAO shall serve the notice u/s 143(2). JAOs shall upload underlying documents on the basis of which notice u/s 148 was issued.

(ii) Cases other than search/seizure/survey, where notice u/s 148 has been issued and proceedings are to be completed on or before 31 March 2027: DIT(Systems) shall forward these cases to NaFAC for further action. Notice u/s 143(2) will be served through NaFAC.

Entities whose registration or approval under sections 12A, 12AB, 35(1)(ii)/(iia)/(iii), 10(23C)(iv)/(v)/(vi)/(via) etc. has either:

(i) Not been granted, or has been cancelled/withdrawn on or before 31 March 2025; AND

(ii) The assessee has been found to be claiming tax-exemption or deduction in the return filed in ITR-7.

Where withdrawal orders have been reversed/set aside in appellate proceedings, those cases will NOT be selected.

Cases where an addition in an earlier assessment year on a recurring issue of law or fact (including transfer pricing) is:

and where such addition has become final (no further appeal preferred), or has been upheld by Appellate Authorities in favour of Revenue.

(a) Specific information pointing to tax evasion is provided by any law-enforcement agency, Investigation Wing, Intelligence, Regulatory Authority, etc.; AND

(b) The return for the relevant assessment year has been furnished by the assessee.

Important: Returns filed in response to notice u/s 142(1) issued in connection with NMS Cycle/AIS/SFT/CPC-TDS/I&CI information will NOT be taken up for compulsory scrutiny unless independently falling under CS 06.

The circular carves out a distinct procedure for Assessing Officers in International Taxation and Central charges. Such cases may be selected for compulsory scrutiny following the same parameters, but with prior administrative approval of Pr.CIT/Pr.DIT/CIT/DIT concerned. These cases shall continue to be handled by International Taxation and Central Circle charges respectively.

Notably, the requirement to communicate with NaFAC for access and further action after selection does not apply to these charges.

For tax practitioners and compliance teams, these guidelines serve as an early warning system. Returns falling under any of the six parameters should be prepared with thorough documentation well in advance of the June 30, 2026 deadline.

Assessees covered under CS 05 should be particularly alert: the Pr.CCIT must transmit the consolidated list to DIT(Systems) by 15 June 2026 — just a fortnight before the notice issuance deadline.

The expansion of NaFAC’s role for CS 03(ii), CS 04, and CS 06 continues the department’s push towards faceless assessment. For assessees in search and survey cases (CS 01 and CS 02), however, the more traditional jurisdictional route with Central Charge transfer requirements remains operative.

Tax advisors should also note that the 15-day transfer window for cases outside Central Charges applies across CS 01, CS 02, and CS 03 — missing this window could create procedural complications in assessments.

We wish to consistently build value for our clients by delivering a motivated and committed team of professionals working hand in hand to maintain the highest standards of integrity and confidentiality in fulfilling client-specific needs.

This will close in 0 seconds

WhatsApp us