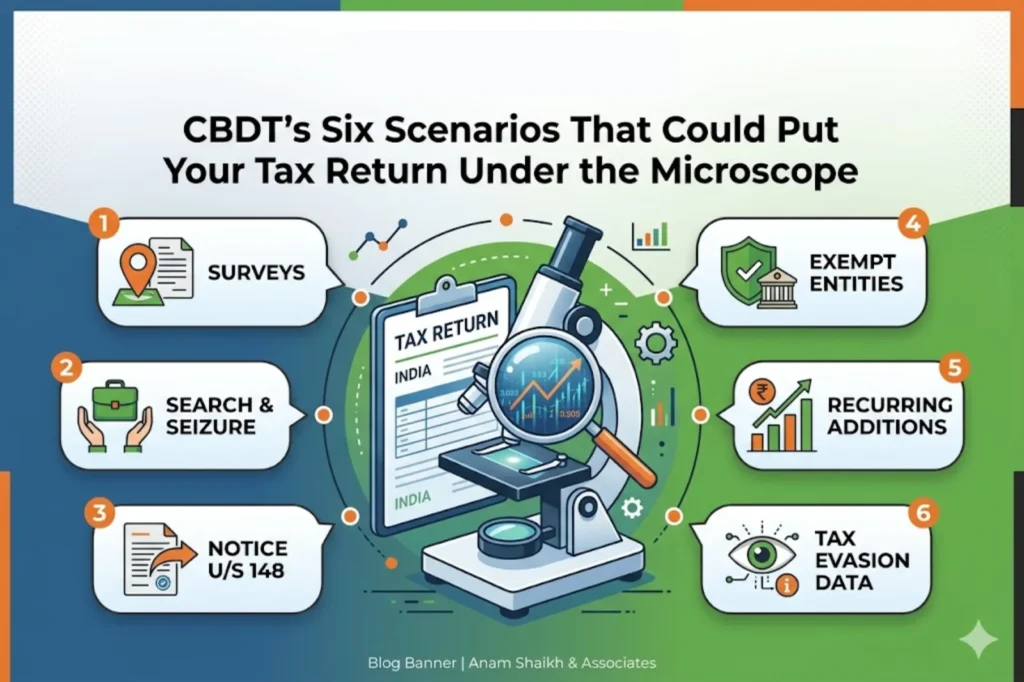

CBDT’s Six Scenarios That Could Put Your Tax Return Under the Microscope

Helping Startups Manage Finance, Compliance & Growth

04/27/2026

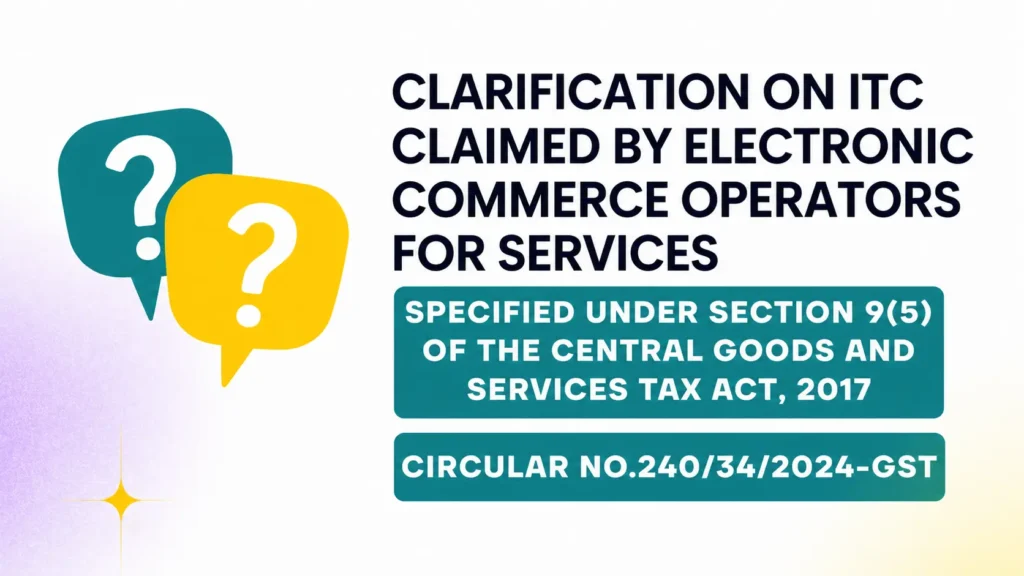

Reference is invited to Circular No. 167/23/2021 – GST dated 17.12.2021 whichclarified that electronic commerce operators (hereinafter referred toas “ECOs”) required to pay tax under section 9(5) of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as “CGST Act”) are not required to reverse input tax credit (ITC) in respect of supply of restaurant services through their platform (notified services under section 9(5)). In

this regard, representations have been received seeking clarification regarding requirement of reversal of ITC, if any, in respect of supply of services, other than restaurant services, under section 9(5) of CGST Act.

The issue has been examined and to ensure uniformity in the implementation of the law across the field formations, the Board, in exercise of its powers conferred under section 168(1) of the CGST Act, hereby clarifies the issue as below:

Issue

Whether electronic commerce operator, required to pay tax under section 9(5) of CGST Act, is liable to reverse proportionate input tax credit on his inputs and input services to the extent of supplies made under section 9(5) of the CGST Act.

Clarification

We wish to consistently build value for our clients by delivering a motivated and committed team of professionals working hand in hand to maintain the highest standards of integrity and confidentiality in fulfilling client-specific needs.

This will close in 0 seconds

WhatsApp us